Beer Marketer's Insights

Monster net sales from alc bev brands tripled to $46.3 mil in Q1 2023 vs $15.2 mil year ago, co reported late afternoon yesterday. Recall, sales from Q1 2022 only included CANarchy brands after closing the acquisition on Feb 17. So this yr's sales include an incremental 1.5 mos of CANarchy brands plus initial Beast Unleashed launch, which totaled $20.5 mil in Q1, co-ceo Rodney Sacks shared. Suggests CANarchy portfolio posted $25.8 mil in 3 mos of 2023 vs $15.2 mil in 1.5 mos, still getting dragged its by hard seltzers and craft brands other than Cigar City and Deep Ellum. Tho co "recently relaunched Wild Basin Hard Seltzer" with new packaging and flavors and refreshed Oskar Blues Dale's brand with plans to intro new Dale's American Light Lager, Rodney noted.

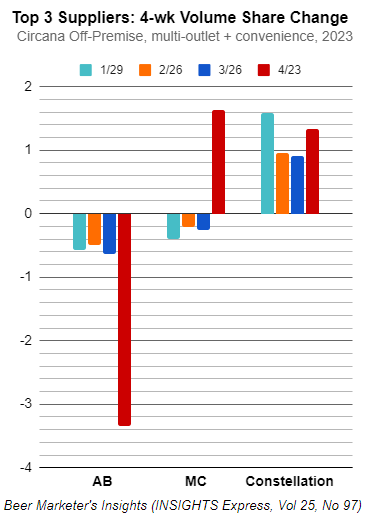

AB Under 40 Share of 4-Wk Off-Premise Cases in Circana, Modelo Especial Within 1 Pt of Bud Light $$

AB shed 3.3 share of beer industry volume to 39.7 for 4 wks thru Apr 23 in Circana multi-outlet + convenience data. Based on 9.4% decline, AB's 4-wk share loss was 5-7x its 0.5-0.6-pt dips in prior periods (see chart below). Molson Coors went from losing 0.2-0.4 share of volume to picking up 1.6 share last 4 wks, hitting 22.4 share on 5.9% volume gain. And Constellation picked up more share than it had been, +1.3 to 14.4 share as volume jumped 8.1%. By $$, AB off 5.4%, while MC almost matched Constellation's growth rate, +11.5% and +12.4%, respectively. In fact, if MC had shed same 0.2 share of $$ it lost the prior 4-wk period thru 3/26, Constellation would've passed it to be #2 brewer by $$ in scans.

Two suburban NY wholesalers on either side of Mario Cuomo Bridge will combine as 3.3-mil case Dana Dist (including NAs) in Goshen NY will buy 1.5-mil-case D. Bertoline & Sons in Peekskill, NY. So Dana will be close to 5 mil cases. Bertoline almost all AB. Deal expected to close in next month or so.

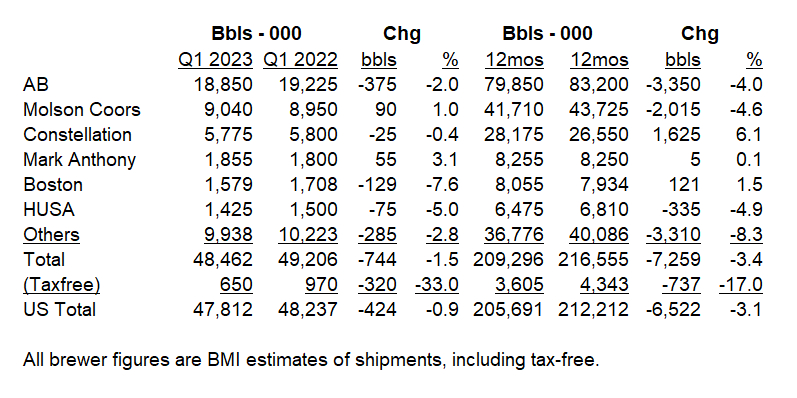

Beer shipments remained soft in Q1, tho much improved vs big drops thruout 2022. US shipments slipped a little less than 1%, INSIGHTS estimates based on Beer Inst, TTB and US Dept of Commerce data. Total shipments softer including steep export drops as top brewers are seemingly shifting more production of international volume to mkts outside the US.

Beer's US consumer base continues to wane. A projected 92.6 mil American adults drink beer, expansive MRI-Simmons USA survey found in latest results. That's 38.4% of all 21+ adults, around 61.5% of all drinkers and sounds impressive enough. Until you compare to spirits, consumed by about 119.8 mil Americans, 49.7% of adults and 79.6% of drinkers, these surveys show. That's equivalent to a 27-mil-person gap between US beer and spirits drinkers. Almost 58 mil Americans drink, just not beer.

MC Q1 Depletions Remain Soft in US, But $$ Keep Growin'; +10% in Apr Scans vs Bud Light Drops

Molson Coors posted its 8th straight qtr of revenue growth and grew bottom line by high double-digits in Q1 2023, co reported earlier this week. That includes sales up 5.6% to $1.94 bil, shipments down 0.5% to 11 mil bbls and income before taxes soaring up 168% to $233.4 mil in Americas region (primarily US, plus Canada and various countries in Caribbean and Latin/South America). In US, MC's 1% shipments gain was ~4 pts ahead of depletions, which slipped 2.8% selling-day adjusted, cfo Tracey Joubert shared on earnings call. (Reported depletions were -1.2% with 1 extra selling day.) Co intentionally built inventory ahead of depletions to avoid supply chain disruptions that became common these past few yrs in Q1, ceo Gavin Hattersley explained. Yet MC STRs still soft to start the year.

AB sales-to-retailers down 3%, but revs up 4%, with rev and EBITDA flat thru 1st qtr in US. That's pretty typical qtr for AB in US. And global ABI posted strong results, revs and EBITDA each up double digits. But ongoing Bud Light controversy overshadowed strong global results. All eyes on April and Q2 trends, wondering how long this will continue.

US beer volume remained soft in Q1. US shipments slipped about 1%, INSIGHTS estimates, including taxpaids down 1%, imports up 1%, domestic hard cider down low-to-mid-singles and domestic NA beer up double-digits. Total shipments slipped at a steeper rate including sizable export drops. US depletions were also down a little more than 1% for the qtr, including 5% drop in Mar, Beer Inst estimates. But $$ remained far healthier and growing with fall price increases still factored in and beer prices up 7% in Q1 CPI data.

INFLUENCERS: Coco5! Coco5! Lakers' D'Angelo Breaks Down Grizzlies Game: 'Coco5!' - 'Leave It!'

A week ago we noted retirement after distinguished career of Chicago Blackhawks trainer Mike Gapski, who'd devised coconut-water based Coco5 hydration brand that's now being operated by investor Jim Lawrence and raft of hoops stars led by Suns' Devin Booker (BBI, Apr 25). Those investor/endorsers have been raisin' a ruckus behind brand, occasionally with viral results. Case in point: Lakers/Grizzlies postgame presser by Lakers' D'Angelo Russell in which he gleefully violated team policy by touting unauthorized Coco5 brand while Lakers or NBA apparatchik ordered him to stop. "You gonna have to fine me," he said. "You gon' have to take it," which the woman did, as Sports Illustrated reported. As Yahoo Sports noted, Gatorade is official sports drink of NBA while BioSteel was named official sports drink of Lakers in 2021. When presser concludes, Russell chants, "Coco 5, Coco 5 . . ." as official tells him to "leave it." "Can I see my bottle?" he demands. "Where's my bottle?" "New flavor loading . . . 'Fines Paid,'" brand posted soon after. Postgame event has been viewed over 1 mil times by now.

To mix of fascination and skepticism, Chicago-based Foxtrot Market has been pushing envelope of what c-store can be, curating mix of mainstream and oddball offerings to affluent urban shopper base while building ecomm in from start. In interview with trade letter C-Store Dive, its recently elevated ceo Liz Williams, a restaurant vet, indicated that co has slowed its openings a bit as it focuses on refining model but is eyeing first move into suburban locations. It's also building out its private-label offerings and seeking to maintain careful balance between cutting-edge brands and familiar, mainstream brands - as our own check this wk of Chicago location confirmed. Backed by private equity, chain operates 26 locations in Chicago, DC/Virginia and Texas. Williams arrived as prexy/cfo a year ago and was elevated to ceo last month, as founder Mike LaVitola segued to chmn role.