BMI Archives Entry

MC hired Michelle St Jacques, its first female chief marketing officer starting Feb 4. Last cmo David Kroll left back in Jul. Michelle previously SVP and Global Head of Brands at Kraft Heinz where she led turnaround of Heinz brand and others with outside-the-box mktg. Undoubtedly, she brings fresh perspective. But she inherits an unsettled mktg deptthat’s had a lot of turnover, not many wins and lack of bench strength in recent yrs. MC cut MG&A costs by $75 mil thru 9 mos 18, including mktg cuts and this yr it will get many millions less in local mktg from distribs looking to recoup increased freight and fuel charges. Yet MC execs, even ceo Gavin Hattersley, have talked up MC’s “big marketing plans” for 2019. MC uses its “Behind the Beer” blog to get message out. “MillerCoors is ramping up its marketing spend” read one post, “plans major digital marketing investments.” MC will double spending on Blue Moon, Peroni, Arnold Palmer, also “making big bets” on Cape Line, Henry’s Hard Sparkling. Peroni will get first natl ad campaign. Each of those above-premium products, where MC under shared and losing share. Coors Light also has new campaign and will be “investing more in social media” including big jump on “non-linear TV platforms” like Hulu, Netflix, Amazon, Roku, YouTube, MC said. Those jumped 50% to 13% of total viewing last yr, said MC blog, while “tv ratings remain down double digits.” But “that’s not to say MillerCoors is walking away from TV. Far from it.” Still, given MC declines and financial targets, safe to assume it won’t be increasing every aspect of mktg. For example, just lost naming rights to Miller Park to American Family Insurance in Milwaukee. It passed on several sponsorships in recent yrs. But MC’s tone, mktg ambitions, new cmo show it fighting to get back on track.

Steady stream of AB news on pricing, mktg, finances led up to SAMCOM meeting with distribs in Dallas. AB will take natl price hike Apr 1. And AB will take price in spring from now on, in break from past practice. Meanwhile, starting in Feb, Bud Light will include ingredients on labels. It advertised that move heavily on high profile platforms like NFL playoffs. AB buying 5.75 minutes on Super Bowl, more than it has in yrs, featuring 7 brands. Already shared Bud, Bon & Viv and Mich Ultra ads with media, while teasing Stella. Both Bud and Stella featured community-minded ads on issues like sustainability and providing water to those in need. Meanwhile, ABI’s $100 bil in debt and lack of clear growth/margin prospects led to wildly divergent reports from financial analysts; some downgraded ABI stock using harsh language, while one said debt concerns “overstated.”

Big news at presstime: on eve of SAMCOM, AB resolved major issue with many distribs as it rescinded its planned 6 cent freight surcharge, sources say. It had wanted distribs to eat 6 cents/case. Many balked. Instead, now AB will just take price hike Apr 1 with normal 70/30 split. “Finally they listened” to distribs, said source. This will make for much improved meeting in Dallas. No official word yet from AB at presstime. But Wow!

Bud Light will be first major beer brand to put nutrition panel on labels “because it’s the right thing to do,” one ad sez. Yet there’s competitive angle too. This puts additional pressure on craft, wine and spirits brands (frequently far higher in calories), sources say. Bud’s Super Bowl ad returned to Clydesdales, dalmatians and Western scenery, but with sustainability twist: “Now brewed with wind power for a better tomorrow,” sez ad. Stella using Sarah Jessica Parker on “Pouritforward” campaign (buy a Stella and 1 person gets 1 month of clean water). These messages take activist stance about ABI doing good. But will they lead to better sales? Meanwhile, AB up 0.4% for 4 weeks thru Jan 12 in Nielsenall outlet. It lost 0.5 share of volume, compared to 0.7 in 2018.

Plenty of financial news popped too. ABI reportedly “considering” partial IPO in Asia and it also issued $15.5 bil in debt of longer duration, two measures to ease its debt burden. New bonds have 40 yr maturity, “kicking the proverbial can down the road,” said Bloomberg. Some viewed both moves as trading better assets for less good ones. Yet RBC’s James Edwardes Jones countered that “the dangers of AB InBev’s indebtedness have been overstated” and debt “should be manageable from operating cash flow.” Bernstein’s Trevor Stirling viewed both moves as positive to “de-risk” the biz. Still, all this focus on ABI debt clearly conveyed co in very different place than 2 yrs ago when all the chatter was about who it would buy next.

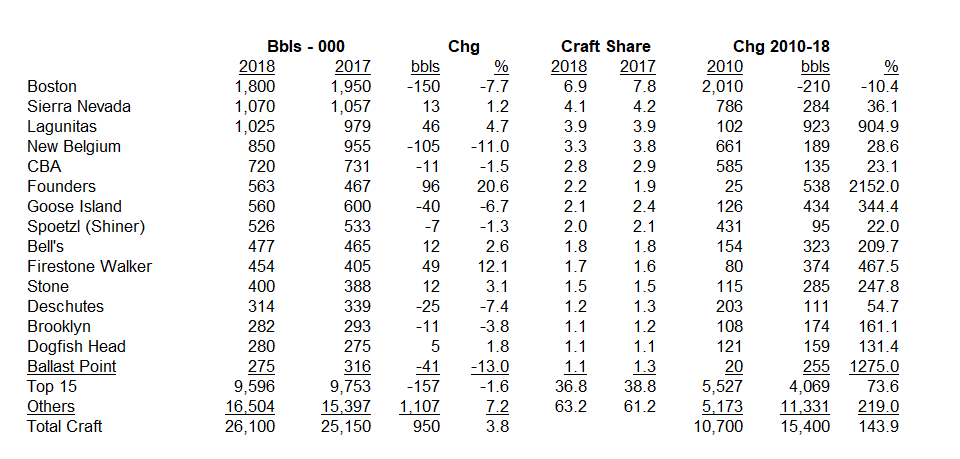

A bumpy road, but craft beer still managed to grow almost 1 mil bbls in 2018, we estimate, up near 4%. That was craft’s smallest volume gain since 2009. Craft growth exploded in 2010, grew double-digits for next 6 yrs. Those were go-go yrs. But craft ain’t what it was. Many of largest craft brewers slowed/declined as most craft growth from thousands of small local players and/or own-premise. FMBs and imports grew faster than craft in 2018.

Eight of Top-15 Craft Brewers, 3 of Top-5 Flat-to-Down It ain’t easy being a top-tier craft brewer. Of top 15 craft players, 8 ended 2018 flat or down, including 3 of top-5, 5 of top-10. Boston Beer’s beer (mostly Sam Adams) declined 8%, we estimate, even as total co likely up about 15% (suggests Boston’s craft biz shrunk to just 42% of its volume). Sierra Nevada up just 1.2% to 1.07 mil bbls. New Belgium took tuff 11%, 100K-bbl shipments hit. After growing 880K bbls over 7-yr span, Lagunitas finished flattish in US last yr, we estimate. But co cracked 1 mil bbls, +5%, including bustling intl biz up 90%. CBA and Shiner each dipped low-single-digits, while Deschutes and AB’s Goose Island each off high singles and Constellation’s Ballast Point declined double-digits for 2nd straight year. So, top indie brewers and big brewer partners alike struggled in segment.

Founders Got Largest Bbl-Gain (Again); Firestone Over 450K Bbls Only 2 top-15 craft brewers grew double-digits (compared to 8 just 3 yrs ago). Continued growth of Founders and Firestone Walker stands out as segment tightens up. Founders posted largest single bbl-gain in craft for 2d straight year. Up 21% to 563K bbls. Passed Goose and Shiner to become 6th largest craft brewer behind CBA, even as trend came in 10+ pts slower than initial projection. Firestone picked up pace toward end of yr, finished at 454K bbls, +12%.

Mixed Bag Below as Share Shifts Further to Long Tail Other top craft brewers that grew at all mostly grew low single-digits. Bell’s and Stone each up 3% or so. And no one’s grumbling about +3% these days. Just 3 other craft players over 200K bbls in 2018, we estimate. New Glarus also up 3% and SweetWater flattish. But #2 AB-acquired craft brand Elysian flew in scans last yr, blew past 200K-bbl mark, we estimate. All told top-15 craft players collectively down over 150K bbls, 1.6% in 2018. Shed 2 share of craft. Smaller players got that and then some. Trends among vast array of 7K+ remaining craft players even more mixed. But they netted solid growth, gained share, toward 2/3 of segment. Back in 2010, a very different top-15 were majority of craft volume, had near 60 share. That flipped as segment expanded. Now it’s a whole different ballgame.

Taxpaid shipments by domestic brewers declined 3.6 mil bbls, 2.1% in 2018, estimates Beer Inst economist Michael Uhrich. Dec shipments up estimated 278K bbls, 2.2%, offsetting little of 1.5-mil-bbl Sep-Nov decline. Last time domestic taxpaids dipped 2% or more: 2017. Before that, you’re looking at the 1950s. With anticipated import gain, (+4.5% thru Oct, Nov-Dec not yet in), total US shipments down 1% or so, again similar to 2017.

Total bbls figure still up in the air, beyond missing import final. Michael pegs domestic taxpaids at 166.6 mil bbls for 2018. That’s lower than any year since 1970s. But gotta note: TTB hasn’t put out “official” taxpaid number since Jun 2018 to benchmark against and lotsa hard-to-measure beer flows thru taprooms. Then too, TTB removed nearly 500K bbls from its 2017 number before it went dark. So, both 2017 and 2018 figures a bit wobbly and there could be reset down road. No matter what, 2018 will be 6th-straight decline for domestic brewers’, 9th in last 10 yrs and 2d-straight decline for US total of 1% or more. Meanwhile, wine even/up slightly in 2018, spirits lookin’ at another +2%.

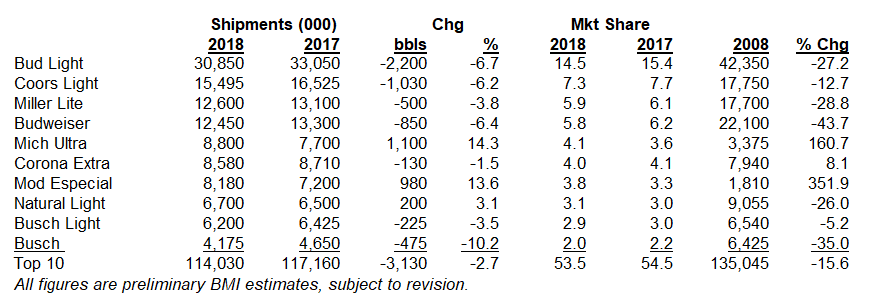

Big mainstream brands in US took big hits in 2018, continuing a very challenging decade. Indeed, 2 of ’em − Bud Light and Miller Lite − each lost over 1/4 of their volume since 2008. Bud lost over 40% of its US/export volume, while growing globally. While Coors Light had best record since 2008, losing “just” 13% of its volume, its dropoff steepened in recent yrs. (Coors Light up 2009-2012, down or flat each yr since). Indeed, these 4 brands collectively lost over 4.5 mil bbls last yr, we estimate, yet are still 1/3 of biz. They’re down a staggering 28.5 mil bbls since 2008. One look at these long-term trends helps explain why AB and MC pivoted more to above-premium and niches, tho each still has to try to turn mega-brands too. Two other top-10 brands in similar 10-yr slide as Bud Light and Miller Lite: Natty Light and Busch. Fast-growing Michelob Ultra and Modelo Especial, plus other gainers and craft in interim, just don’t generate enough volume to offset losses. As result, total shipments about 6 mil bbls lower in 2018 than in 2008.

In 2018, Bud Light down estimated 2.2 mil bbls, 6.7%, its largest % decline on record. Fell below 15 share. Bud Light lost 5 share in 10 yrs. Coors Light just as soft: down 1 mil bbls, 6.2%. Lite did best of the 3: down 500K bbls, 3.8%. Lite gained share of premium light biz, and passed Bud as #3 brand overall (it had passed Bud in US in 2017). But Lite still lost share of total biz, now down to 6 from over 8 in 2008. Bud continued down mid-singles, dipped below 6 share. Hard to believe that at one time Bud alone had over 25 share of shipments (30 yrs ago in 1988).

Two big winners in top 10 each gained about 1 mil bbls, 14% in 2018. Michelob Ultra tacked on another 1.1 mil bbls last yr, we estimate, passing Corona Extra for #5 spot. Modelo Especial closing on portfolio-mate Extra as well (it passed Corona Extra in off-premise scans). Especial up another 980K bbls, 13.6%. Corona Extra dipped 1.5% as Familiar and Premier cut into its volume. Even so, and with Corona Light suffering near-double digit decline, Corona franchise expanded by over 1 mil bbls, over 10%. Natty Light posted its first gain since 2009 as its avg prices dipped about 45 cents/case in scan data. Busch Light down 3-4%, but Busch suffered a double-digit decline.

Off-premise scan data further shows continued erosion of top mainstream brands. Top 4 brands shed 1.8 share of volume and $$ in Nielsen scans for calendar 2018. Among top 20 mainstream brands (in premium or economy segments), only ones to gain volume share were Natty Light and Key Light. Not a single top mainstream brand gained share of $$. Meanwhile, Michelob Ultra and Modelo Especial combined to gain 1.1 share of scan volume, 1.3 share of $$. Otherwise, biggest share winners (0.2-0.4) were still-small brands: Corona Premier and Familiar, White Claw and Bud Light Orange.

Two high-stakes cases in high courts right now. On Jan 16 US Sup Ct will hear arguments over whether Tenn can require 2-year residency for liquor store licenses. US District and Appeals Cts tossed law after mega-retailer Total sought license; Tenn retailers want it restored. Sup Ct got 25 briefs to wade thru weighing issues around dormant Commerce Clause, 21st Amendment and Privileges and Immunities Clause (which bars states from discriminating vs out-of-state citizens). Total gets half-hour to make its case; Tenn retailers have 20 mins, IL AG 10 mins. Beyond residency law, decision could impact states’ rights to bar out-of-state retailers from shipping across state lines, and more. NBWA’s Alcohol Law Review reminds that while Total sez it’s not attacking the three-tier system “it is hard to see how a victory by them would not be used to further this attack” given recent fed ct decisions supporting cross-border shippers. Meanwhile, MC’s match and redirect, and other biz transfer provisions, still on table in US Dist Ct in Nevada. Fed judge refused to declare those provisions violate Nev franchise law and force fast approval of its deal to sell to Southern Glazer’s vs MC choice Breakthru. But he allowed Bonanza to file amended complaint, which now stresses that process “unreasonably delays” deals, illegally allows MC to “dictate” the process and by the way, violates Nev franchise law.

Save the Date: The 2019 Beer Insights Spring Conference will be held in Chicago May 15-16 at the Ritz-Carlton Hotel. Program details coming soon.

Best Wishes,

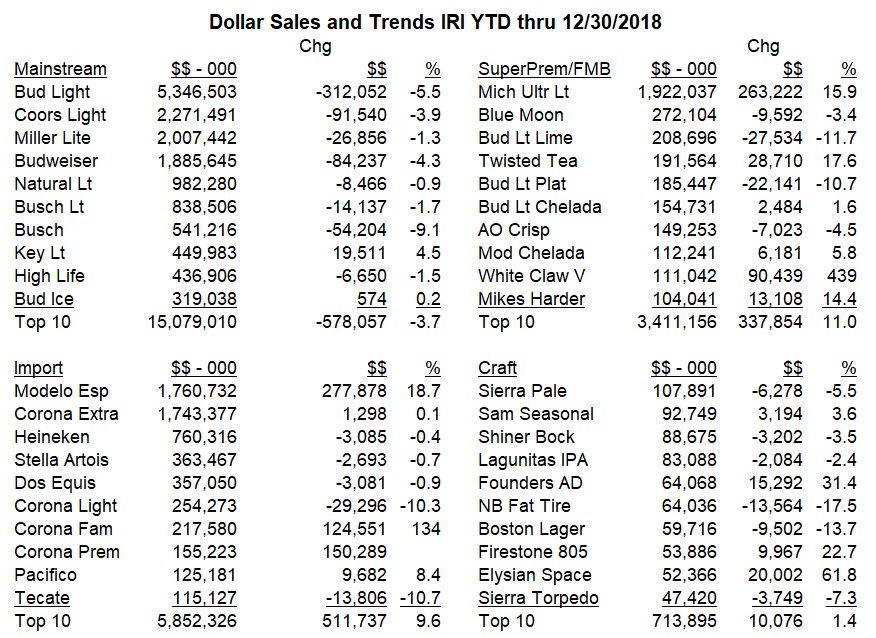

Top 3 light lagers collectively shed $430 mil in IRI MULC scans in 2018, with Bud Light $$ sales –5.5%, Coors Light -3.9% and Miller Lite -1.3%. Volume trends even softer. Only 1 top-10 mainstream brand built $$ sales: Key Light up almost $20 mil. (Natty Light volume up, but $$ down.) Indeed, below top 3, mainstream brand sales off another $150 mil, with Bud over half of that. So top mainstream brands dropped staggering $578 mil in 2018 scans. Even so, total beer $$ sales up $619 mil, almost 2% in IRI. Numbers much better above premium, of course. Some highlights:

- Ultra tacked on $263 mil, 16%; passed Bud as #4 brand in $$ sales, closing on Lite.

- Modelo Especial passed Corona Extra, not far from passing Bud, likely in 2019.

- Corona Family at $2.4 bil, ahead of #2 brand Coors Light.

- Twisted Tea is top FMB brand and #4 brand in combo-segment of superpremiums/FMBs.

- Heineken, Stella and Dos Equis each lost roughly same amount of $$ in scans.

- Six of Top 10 craft brands down in $$. Big winners: Founders All Day IPA, Firestone 805 and Elysian Space Dust IPA.

Not best way to start the yr, but some stubborn trends/facts suggest biz ain’t gonna get any easier for industry’s biggest brands in 2019. Four brands, Bud Light, Bud, Coors Light and Miller Lite still over 1/3 of biz and collectively declined mid-singles in 2018, likely dropped over 4 mil bbls between ‘em. (See next issue for our detailed brand estimates.) Call this a reality check and us bad news bears, but gotta keep this in mind.First and foremost, category ain’t healthy and biggest brands bear the brunt, perhaps disproportionately; they’re all down already for yrs. MC and STZ both reportedly forecast steeper 1.5-2% drop for beer biz in 2019. Secondly, there’s more innovation and fragmentation than ever. And some of it aimed squarely at premium lights. Take seltzers for example. With such similar ABV, calories and sessionability, yet different taste, they aim squarely at heart of premium lights. Both Mike’s and Boston expect seltzers to grow 2 mil bbls in 2019. If so, that puts a ton of extra pressure on premium lights.

Third, tho dust hasn’t yet settled, AB and MC’s freight and fuel surcharges will lead to additional price hikes in marketplace (already have in some places). With their high debt loads, each of AB and MC will be less inclined to discount their biggest brands. Given higher prices, less discounting going against already weakened brand equities, what do you think will happen? Trends ain’t likely to get better. That’s especially true because mktg $$ will likely decline on these big brands. Recall, some big distribs, especially on MC side, reducing local spending. Lots. To offset freight and fuel surcharge. Then too, AB spread its Super Bowl spending across 7 different brands and deemphasizing Bud Light in other ways, according to many reports. MC sez it’s spending will be up in 2019. That would be a switch. MC reduced mktg gen and admin by $125 mil in last 6 qtrs (good chunk mktg). Then too, for some time mktg for top brands has not set world on fire or changed trajectory of these big brands. Throw in increased emphasis on brands that are doing well (like Ultra), plus innovation and distribs gotta face prospect that all this adds up to potentially even softer trends for biggest brands. Finally, spirits, wine and cannabis ain’t goin’ away.

How could that be? Constellation Brands, the one big co in struggling beer biz that’s crushing it, leading all others with near 2-mil-bbl growth in 2018 (see above), reports another qtr of outsized sales gain. Yet stock fell 12% in 1 day. Go figure. It did bounce back 6% next day. But despite STZ’s continued strong beer growth, Constellation results raised lotsa questions from slight beer slowdown, to a little lower margins, reduced earnings guidance, poor wine and spirits sales and how it will account for Canopy. Basic takeaway: more uncertainty about Constellation’s best-in-class results combined with lotsa non-beer issues to make investors more skittish about stock. Is story fraying a little around edges? To counter that thought and boost interest in stock, Constellation pounded theme that it will return $4.5 bil to shareholders over next 3 yrs in form of dividend and share repurchases. But that’s not about growth.

So let’s talk growth. Depletions up 7.8% for qtr thru Nov, now up 9.4% for 9 mos. Constellation shipments up 610,000 bbls, 14% in Q3 alone, up 1.6 mil bbls, 10.2% for 9 mos, 1 point ahead of depletions. That’s pretty great in an industry that’s gotten tuffer. And perhaps there’s the rub. Some think beer biz will be down 1.5-2% in 2019 and that means Constellation growth might “only” be 6-7%. Then too, there’s Corona conundrum. Super successful line extensions (Familiar and Premier) in 2018 led to outsized Corona franchise growth. Up 8% for 9 mos, near 2x rate of previous fiscal yr. Premier did 2x what STZ expected, and still has “ample runway.” But Corona Extra and Corona Light dropoffs steepened in scan as yr went on. Down 4.2% and 17.6% respectively for 12 weeks thru 12/30 in IRI MULC. Another extension, FMB Refresca, will complicate portfolio further and cannibalize some, tho STZ sez it’s 80% incremental. Between tuffer industry, law of large numbers and lapping big intros last yr, Constellation could slow a point or two and still wildly outperform beer biz. But even that prospect spooked Street somewhat.

Strong Oper Income But Slightly Lower Margins; Mexicali? Plenty of Capacity for Yrs Constellation beer operating income up $56 mil, 14% in Q3 and $140 mil, 10% to $1.6 bil for 9 mos. Super strong, but boosted by extra shipments in qtr, 6 pts ahead of depletions. In last qtr of STZ fiscal yr (thru Feb 19), “volume growth will lag depletion growth... due to timing and a tough compare,” cfo David Klein said on call. In Q3, operating margin decreased 60 basis pts to 37.3% because of higher transportation costs (160 basis-pt drag) and marketing investments that jumped to almost 11% of sales ($130 mil). Addressing yet another recent concern, incoming Constellation ceo Bill Newlands responded to reports of political and water issues with its Mexicali brewery. STZ has “plenty of beer capacity in Mexico for the foreseeable future,” is “totally in compliance with all Mexican law” and has “deep understanding” of Mexican water issues. “We do not believe this is a major issue” and “all is going to proceed as planned,” added Bill. But Mexicali “facility will only represent 10% of our capacity one way or the other.” Between Nava and Obregon, Constellation can make 400 mil cases, around 29 mil bbls, enuf for yrs to come.

Wine & Spirits and Canopy Losses? “Total Overreaction” on Stock, Sez Rob; Analysts Other concerns beyond beer biz operations. Constellation low-end wine/spirits biz deteriorating and tho it’s exploring strategic options, so far STZ not finding buyer, or at least at right price. Effect of $4 bil Canadian cannabis co Canopy investment on results will be “non-cash” item and not incorporated yet. But “potential Canopy losses” present “further downside risk,” sez Macquarie’s Caroline Levy. Even longtime STZ fan, Mad Money’s Jim Cramer, referred to “some real hair on the results” citing several of these factors. But Constellation ceo Rob Sands said of stock drop: “I think it’s a total overreaction.” Many Wall St analysts agree: “Selloff Way Overdone,” said Wells Fargo’s Bonnie Herzog; “We Like STZ Here Despite the Q3 Hiccup,” said Morgan Stanley’s Dara Mohsenian, adding “Stock Reaction...Overblown”; “Is the Sky Really Falling?” asks RBC’s Nik Modi (he sez no). Evercore ISI’s Robert Ottenstein also sees more than 20% upside in stock, but “Uncertainties Obscure Compelling Value,” he wrote, pointing to all these factors and adding these are “likely to be overhangs, until the market has greater visibility.”

How tuff was 2018 for US beer biz? Final figures not yet reported, but looks like total US shipments down 1% or more, about same as 2017, following 3 straight gains 2014-2016. Final figure will be lowest in well over a decade, at least 8 mil bbls below 2008 peak. What’s more, US taxpaid shipments – domestic brewers only – look to be down 2% or more for 2d straight year. Yup, domestic brewer trend softer in 2018, following fed excise tax cut, than it was in 1991 when excise taxes doubled! Ironic, but not funny-ironic.

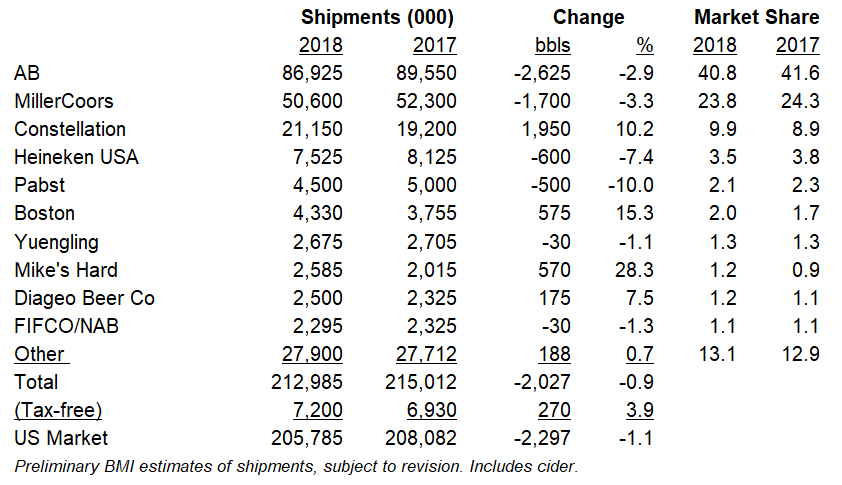

Meanwhile, imports continued mid-singles growth, tho entirely driven by Mexican brands. Trends for top 3 suppliers in 2018, collectively 3/4 of biz, eerily similar to 2017: AB and MC each down in 3% range, we estimate; Constellation up 10%. But some key trend changes below that. Note: these are early estimates; TTB way behind in reporting industry totals and now shut down. No supplier has reported 2018, tho Constellation reported for 12 mos thru Nov. So take ’em with several grains of salt.

With AB and MC each down about 3% for 9 mos, and no signs of improvement (Oct-Dec scans softer), top 2 collectively dropped another 4.3 mil bbls or so in 2018, we estimate. That’s a big hole at the top. Gainers could not offset. (Recall, Constellation believes it will be another few yrs before high-end growth offsets mainstream loss and industry turns positive.) AB share dipped below 41, we figure, down from peak of just below 50 over a decade ago. At same time, AB shed about 20 mil bbls since peak volume in year InBev bought it, 2008. MC dropped nearly 14 mil bbls same period. JV’s peak volume was same yr it formed. MC hasn’t scored up yr since, AB just one. Constellation blew past 21 mil bbls with nearly 2-mil-bbl, 10% gain again in 2018, its 5th straight in double-digitrange while total biz treaded water. Constellation over 10 share of US-only shipments.

That’s almost double since 2007. Tuff year for HUSA and Pabst, tho. Each off at least a half-mil bbls, we estimate. At -7.5% and -10% respectively, much sharper than their 2017 dropoffs. Dipping further into 2d tier, trends improve considerably. Boston passed previous peak (2015) with estimated 575K-bbl, 15% gain, following 6% declines in 2016 and 2017. Boston has solid shot at passing Pabst as #5 brewer in 2019 (already ahead in back half of 2018). Yuengling ended yr slightly down. Despite adding mkts, Yuengling hasn’t scored solid gain since 2014 and remains about 240K bbls below peak.

Lotsa movement among #s 8-10. Mike’s jumped from #10 supplier to #8, passing Diageo and FIFCO USA. Put up monster 28% gain in 2018. Gained virtually same volume as Boston. Collectively, Mike’s and Boston picked up over 1.1 mil bbls. Indeed, current trends have Mike’s already banging on Yuengling’s door. Diageo put up its best gain in over a decade, up mid-to-high singles, we estimate, thanks to firming beer biz, growth in FMBs and seltzers. Mike’s and Diageo each in 2.5-2.6 mil-bbl range. That’s a peak for Mike’s, now on a decade+ roll. But Diageo remains 1 mil bbls below its all-time high. Meanwhile, FIFCO USA shipments off slightly for the year, we estimate, and it slipped to #10.

Looks like All Others, mostly craft, collectively up very slightly, with individual trends all over the lot. Final trend could differ quite a bit depending on final figures for top players and industry total, natch. BA economist Bart Watson expects craft to be +3-4% for the yr. That’s a slowdown from first-half trend of +5%, but better than flattish scan data for segment, as taprooms and newbies continued to tack on volume.