BMI Archives Entry

Indeed, the Lagunitas deal and especially the Ballast Point deal "really screwed up the buy-sell dynamics with at least several companies," said one source, knowledgeable about craft deals. And oh boy, there are a lot more craft deals coming. CBN knows of 10 in play, at least several more in top 50. Presumably there are many more, tho some may not come to fruition (or even become public). Since M&A activity really took off in Sep of 2014, CBN tracked 26 craft transactions (20 in 2015), for part or all of craft brewers. In the last 16 months, 10 of the top 30 did deals of all kinds.

So the craft landscape too has changed utterly. Now each of AB, MillerCoors, Heineken and Constellation Brands have significant presences in segment. Battle lines are being drawn between independent craft brewers and the giants, as our columnist Diogenes suggested last issue. And as our IRI chart in same issue showed, some pretty significant entities are jostling for position within the craft and craft-competing space, however you define the term "craft." Some folks are still likely gonna sail above the fray, with combo of strong local position, great liquids, expansion possibilities and sound management. But others are gonna get bloodied. Craft segment has already entered a new era in its development. Even as overall craft segment growth continues up strong, so far next phase ain't lookin quite so pretty.

Diogenes on Deal Landscape

Our anonymous columnist Diogenes, gives his take on how all the craft deals of 2015 are shaking up the landscape. His perspective is that of a biz insider. His views do not necessarily reflect that of the editors of Craft Brew News. Send your comments to

by Diogenes

Amid a storm of craft brewery deals and the colossal ABI-SAB deal, two-thousand fifteen is raising big questions about the future of the craft beer revolution.

Will the now thousands of small and independent companies that embody this revolution and grew to 12% of the US beer industry (2015 estimate) continue to drive the growth of craft beer or will the international giants buy and own the revolution?

And if the giants win, will it really be a revolution? Does it matter?

Here is a quick rundown of the giants' deals:

-Ballast Point, producing 280,000 barrels this year and growing rapidly, sold to Constellation Brands, importer/brewer of Modelo brands for the USA, for $1 billion.

-Lagunitas, the fast rising #4 craft brewer, sold 50% to Heineken with an option for the world's #3 brewer to buy more, and therefore control. The reported price for half was close to $500 million.

-Three young craft brewers sold to ABI and MillerCoors, proving for the first time that you can "get rich quick" in the craft beer business.

Los Angeles's Golden Road Brewing Co. sold reportedly for over $100 million. Barely four years old, Golden Road will sell about 45,000 barrels this year. Co-founder Meg Gill boldly stated she was throwing in her lot with the "winning team" -- ABI. Nine-year-old 10 Barrel Brewery in Bend, OR, producing 40,000 barrels sold for reportedly near $50 million. (AB also bought Elysian, but they'd been around for significantly longer.)

These young brewers seem to be what the Brazilian billionaires behind ABI call PSDs -- people who are Poor, Smart and have a Deep Desire to get rich. That is the profile that the Brazilian billionaires of 3G Investments look for when choosing partners for their ventures. These are the guys who own a controlling interest in ABI and now are buying SAB Miller.

Also in the get-rich-quick class is 2-year-old St. Archer in San Diego, producing 17,000 barrels last year. It sold for a reported $35-40 million to MillerCoors. Finally, Founders Brewing of Michigan sold 30% to the Spanish brewery Mahou, a big company but hardly a giant.

There were other deals that still qualify as "independent" per the definition of the Brewers Association:

-Firestone-Walker of California joined Boulevard of Kansas City in selling to Duvel-Moortgat of Belgium. Abita sold to the private equity venture Enjoy Beer led by Harpoon founder Rich Doyle. Dogfish did a small private equity deal, selling a 15% stake. There are many similar private equity deals

-Kim Jordan of New Belgium, beneficiary of an ESOP, stepped into the role of executive chair. Kurt Widmer of Widmer Brothers, part of Craft Brew Alliance, assumed a similar role. Deschutes did a small (less than 10%) ESOP. Left Hand and Odell also converted to ESOP ownership.

The employee-owned companies are independent but I wonder about the future of employee ownership. Why wouldn't the employees someday just want to cash out, like the employees of Full Sail of Oregon did when they voted to sell to a private equity company?

What does all this mean? It seems to me the big conflict remains between the international mega-brewers and the small and independent American brewers.

It is clear that ABI, MC and now Heineken and Constellation are committed to playing big in the craft segment. MC already boasts that Blue Moon is the biggest craft brand. Can the big guys dominate the craft segment the way they dominate the mainstream segments?

The number I will be watching is the market share of the big brewer-owned craft beers versus the market share of the independents.

After all, many craft brewers view themselves as part of a revolution in the beer world, a return to distinctive independent breweries that are not owned by the giants that have dominated the US beer industry for decades. Selling out to ABI or MC or Heineken or Constellation only perpetuates the big brewery domination of the industry.

The most important player in this battle may not be the big brewers or the independent brewers. It may be America's beer distributors, the "independent" second tier that many credit with a key role in fostering the craft beer revolution.

Will ABI continue to acquire distributors, even though it said it would cap ownership of its network at around 10% of volume? Will the independent distributors devote an out-sized share of mind to the big brewers and their craft brands, or will they commit to delivering the diverse array of small independent brewers that have led craft growth in recent years?

Three Breweries and BA Named to Outside Mag's "Best Places to Work" List; Odell on ColoBiz List

Folks like working at breweries, it seems. Three top breweries as well as the Brewers Assn made annual list of "Best Places to Work," created by Outside Magazine to highlight companies that value work/life balance. Employee-owned New Belgium ranked 35 and topped the smaller list of "Best Culture Jobs." Outside ranked the BA, another Colo-based co, at #61 (5 on the Culture list), then Ninkasi and Deschutes, a pair of Oreg breweries, at #81 (8 on Culture list) and #95 (10), respectively. A fourth brewery, Odell, topped ColoradoBiz magazine's similar list for mid-sized companies. Note that 3 of these 5 companies are at least partially employee-owned.

At same time, folks behind Dorchester Brewing, a planned smaller contract facility, just acquired a 25K sq-ft space in the co's namesake neighborhood in Boston for $3.3 mil. Founders include ex-Harpoon head brewer Todd Charbonneau and a mktg/ops exec Matt Malloy who recently spent 8 yrs at Zipcar. Both Dorchester and IBG seek to offer more than just production for small companies, including mktg and strategy consulting and tasting rooms to sample beers made on site, natch.

Georgia Press Seeks More Info About Brewery Tour Sales Bulletin; KY Brewers Seek Larger Bbl-Cap

Brewers, of course, remain "disheartened." GCBG exec director Nancy Palmer maintains that whichever entity (DOR or GBWA) initiated discussions over the content of the bulletin, "the result is completely unacceptable," she told AJC. As for uncertainty about effective date in the Sep bulletin, since its release and meetings brewers organized with the governor's staff, the DOR has held an "informative seminar" with brewers that clarifies 2 things: new rules go into effect Dec 1 and if brewers are found in violation, tasting room privileges can be suspended for a year, according to Atlanta Magazine.

In Kentucky, brewers plan to ask for amendment to current definition of "microbrewery" in the state, upping the volume cap currently placed on it. Right now, brewers producing less than 25K bbls per year can operate taprooms. Brewers hope to get legislation passed to double that cap to 50K bbls, according to local Louisville NPR affiliate's report. Interestingly, a pair of Republican state senators told the radio station they'd support such a measure. Sen Damon Thayer noted that "it should not be up to government to set these artificial caps on commerce," preferring instead to "let the market and the free enterprise system decide." Of course, an interest in the free market didn't exactly drive lawmakers to pass anti-branch legislation in the state earlier this year. Recall that small brewers in the state largely backed that wholesaler-driven bid.

NBB with Coors Legacy Network in NJ

New Belgium's distrib appointments in New Jersey coming down the pike and it went with Coors Legacy network there, sources say.

5 More Sens "Concerned" About ABI-SAB, AB Branches; A Bid to Ban Branches from Inside Beltway?

Recall, earlier this month, Oreg Sen Ron Wyden and Conn Sen Chris Murphy separately reached out to the Dept of Justice and FTC raising concerns about pending AB InBev purchase of SABMiller and AB branches curtailing craft access and/or brewing materials. Now, here comes another group of 5 Senators echoing same sentiments to DoJ. But they raise the anti-competitive ante a few notches. In addition to ABI-SAB, Senators Angus King (ME), Jeff Merkley (OR), Susan Collins (ME), Richard Blumenthal (CT) and Chris Coons (DE) are "particularly concerned about large commercial beer companies attempting to gain market share by either purchasing distributors or pressuring distributors to favor their products."

Amid outsized growth of craft in last decade, "large brewers have taken notice and have taken actions that we believe may amount to exclusive dealing and other violations of antitrust law," they wrote. These include: 1) recent purchase of craft brewers by ABI, suggesting "a dangerous plan to constrain distribution channels"; 2) ABI purchases of "one of the two distributors that deliver the vast majority of beer" in any given mkt, forcing remaining brewers out of distribution or into "uncomfortable situation of being distributed by their largest competitor"; 3) in mkts with independent distribs, there are reports that "AB InBev puts pressure on the distributors to favor AB InBev products - a practice that could well be deemed exclusionary and illegal." Therefore, DoJ "should vigorously scrutinize" ABI purchase of SAB so that ABI doesn't increase its "already dominant market position." Even if that doesn't happen, DoJ should "carefully consider" any potential impact on brewing/pkgng materials.

Finally, and here's where the NBWA's fingerprints might be just barely detectable, these Senators want DoJ to "probe how each of these companies has acted with regard to distributors and investigate whether distributors owned by these companies also need to be divested." Sen Wyden's letter had expressed "concern" about reports that AB and its branches "may have acted to curb competition in markets including Oregon" and asked DoJ to "ensure that anti-competitive practices do not recur in the future." But he did not suggest divestiture or use the same kind of antitrust-specific language in this new letter. Perhaps that's because he's the author of "compromise" federal tax legislation that brought BA and BI (and to a lesser extent NBWA) together. Net-net: looks like the battle against branches has escalated beyond state-by-state efforts.

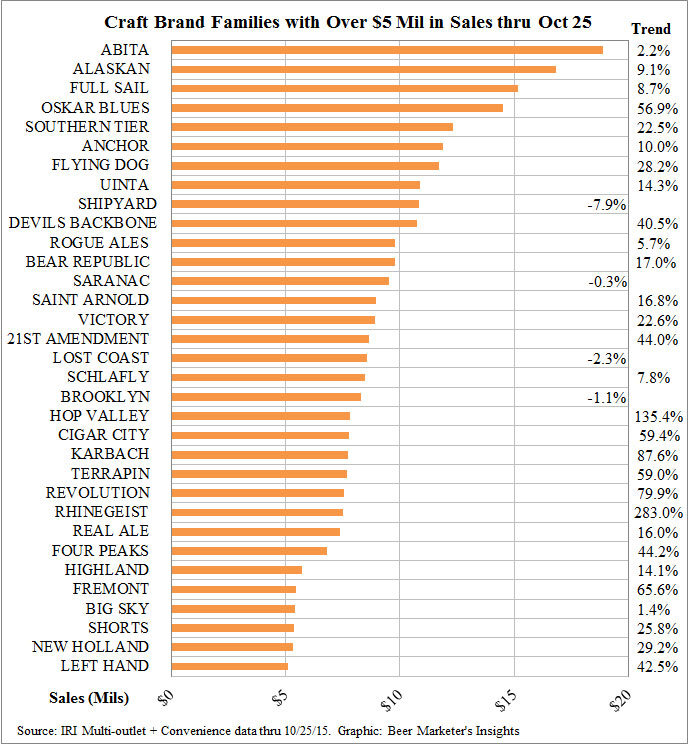

OR's Hop Valley and OH's Rhinegeist are two of fastest trending companies in IRI and leapt into top-50 craft cos this yr. Hop Valley up 135% to $7.8 mil total sales yr-to-date in IRI multi-outlet + convenience data thru Oct 25. Enough to put 'em at 41st largest co in terms of dollars. That's up 19 ranks vs last yr. Hop Valley passed a slew of some of the hottest craft brewers over the last few yrs, including Cigar City (+59%), Karbach (+88%), Terrapin (+59%) and Revolution (+80%). Hop Valley's getting majority (about 80%) of its growth from three IPAs. Both its Alphadelic IPA (+145%) and Alpha Centauri Imperial IPA (+108%) are more than doubling in this yr. And its Citrus Mistress IPA is one of top new brands in scans this yr, already at $1.2 mil thru Oct 25. Seems like every other year there's a new fast-trackin' Oreg brewery.

Meanwhile, Rhinegeist comes in just behind those cos listed above, at #46. That's up a whopping 283% to $7.5 mil YTD. It leapfrogged around 40 cos in the last yr after finishing 2014 as largest newly tracked craft vendor in IRI. Rhinegeist has 4 brands up triple digits, and 3 that are all incremental this yr. While its Truth IPA (+147%) still leading the way, its Franz Oktoberfest shot up most of any of its brands this yr, up 815%. Those two brands together make up over 2/3 of total sales and total growth. Its Cougar Blonde and Zen Session Pale Ale up 182% and 133% respectively.

Several of the usual suspects for posting top trends have slowed some this yr, tho still getting solid growth off larger bases. Devils Backbone (+40%), AB's 10 Barrel (+30%), Flying Dog (+28%), Southern Tier (+23%), Uinta (+14%), Cigar City, Karbach, Terrapin, Revolution (see trends above) and Four Peaks (+44%) all saw trends slowdown a bit. Contrarily, Ballast Point (+154%) and Oskar Blues (+57%) actually accelerated, and Founders (+78%) right around same trend as last yr - three of the largest cos with trends that high, and all of 'em sold part or all of their biz in last yr. New Glarus (+37%) continues to accelerate in latter half of this yr, and 21st Amendment trends rampin' up, +44%, with newfound capacity at its recently opened brewery. Gotta note, a few breweries are down in top-50, including Shipyard (-7%), Lost Coast (-2%) and Brooklyn (-1%).

Also, several smaller cos outside top-50 still zippin' in scans too. OH's MadTree (170%) and WA's Fremont (66%) each grew sales over $2 mil. And plenty grew sales over $1 mil, including two more from OR - Worthy +119% and Laurelwood up 65%. In CA, Coronado up 56%, Drakes up 139%, and MC's Saint Archer up 116%. NY's Sixpoint up 59%, TX's Deep Ellum up 218%, MD's DuClaw (+135%) and WA's Bale Breaker (+221%) all up over $1 mil. In FL, Funky Buddha got an incremental $1.3 mil in sales thru Oct 25. And lots growin' solid double-digits that are up over $1 mil in scans: Shorts (+25%), New Holland (+29%), Left Hand (+43%), Odell (+36%), Foothills (+30%), Smuttynose (+31%), North Coast (+34%), Allagash (+46%). Lastly, a handful of smaller fast growin' brewers to keep an eye on: another OR brewery, Breakside (+162%), DC Brau (+220%), TX's Revolver Brewing (+217%), Montauk Brewing (+107%) and Surly (+361%). Those breweries grew combined $4.6 mil to-date.

Snapshot of Off-Premise Landscape: Portfolio Building in Preparation for Tougher Competition

War metaphors have their uses and their pitfalls when applied to business, but if you believe craft's been a revolution, that battle lines are being drawn or there's a bloodbath coming, here's a look at the relative size of primary combatants to date. Coalitions form as consolidation and category blurring keep complicating any clear measurement of craft and craft-competing brands. Portfolio plays are poised to make a much larger impact as they grow. Yes, these portfolios will keep expanding in both number and size.

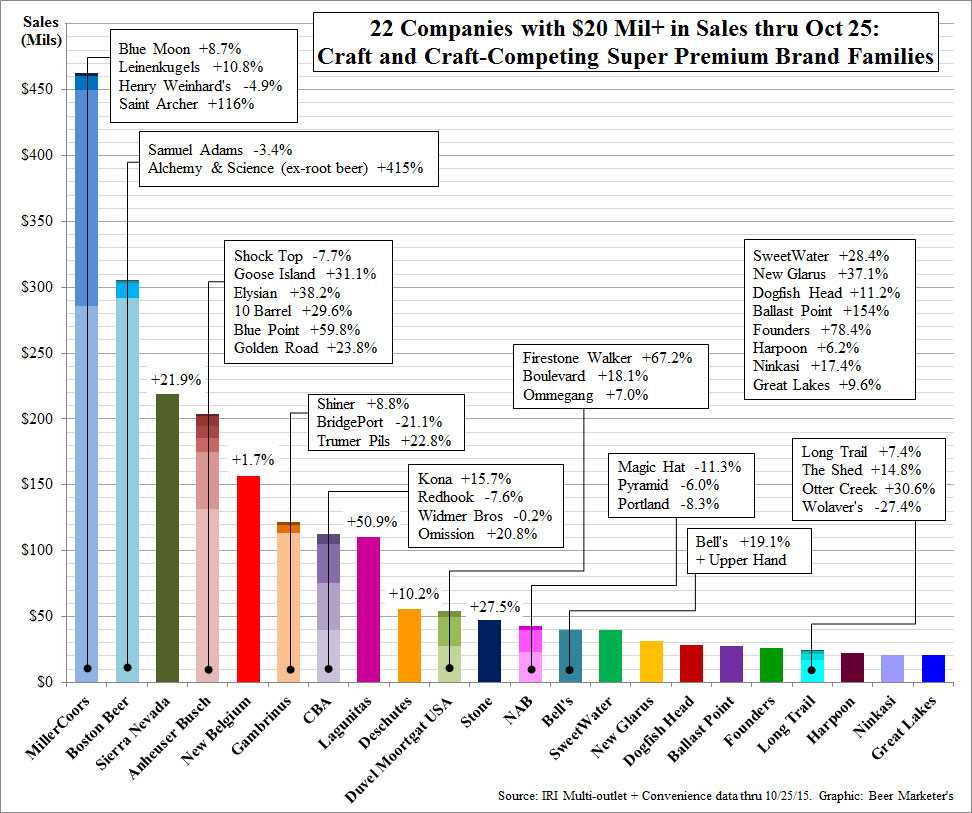

The only transaction that truly transformed an existing portfolio, at least in terms of their size in scanned off-premise channels, was Duvel Moortgat's addition of Firestone Walker. It more than doubled DMUSA's existing craft biz in IRI multi-outlet + convenience data thru Oct 25, adding $27.5 mil in sales to combo of Boulevard and Ommegang at $26.6 mil. At same time, the 4 most recent acquisitions by AB add almost 17% to $$ sales of Shock Top and Goose Island. On the other hand, MC's acquisition of Saint Archer adds less than half a percent to its portfolio of craft-competing super premium brands. This deep dive into IRI's off-premise data notes trends we've reported all year but provides a much clearer picture of what's going on inside these portfolios. Shown below, 22 companies sold over $2.8 bil worth of craft or craft-competing brand families in IRI's multi-outlet + convenience universe thru Oct 25.

Importantly, this analysis does not include other competitive segments like imports, FMBs, cider or hard soda. As such, Lagunitas and Ballast Point are listed separately rather than with Heineken or Constellation. For reference: Small Town Not Your Father's Root Beer sold about $71.3 mil in IRI MULC thru 10/25, so midway between Lagunitas and Deschutes. Also note that for this analysis, portfolios were determined by deals announced to-date, rather than if those deals closed or not. And, as always with this data, remember that it only measures scanned off-premise sales from participating retailers, and therefore trends are not necessarily representative of a company's overall biz.

Only 3 Existing Sam Brands Growing as Boston Beer Boosted by Alchemy & Science Single largest brand family here remains Boston Beer's Samuel Adams portfolio. But it's shrinking, down 3.4%, almost $10.4 mil thru late Oct. New Sam Adams brands adding about $9.9 mil of incremental growth too: over half that is Rebel Rouser Double IPA and most of rest in either session Rebel Rider or Pack of Rebels variety pk. Only 3 Sam brands grew YTD thru 10/25: Rebel IPA up 19%, Seasonal Overlay up 13% and Cream Stout up 7%. At same time, Alchemy & Science subsidiary up 1000% plus, largely thanks to big Coney Island Hard Root Beer launch (excluded in chart, which only shows non-root beer Coney Island brands). Even without CIHRB, A&S up 415%, adding an almost entirely incremental $10.2 mil to Boston total sales during this period, mostly from Traveler shandy brands (see Nov 13 issue for look at A&S sales thru 11/1).

Solid Year for High End MC Biz Total Blue Moon brand family currently just $6-7 mil behind total Sam Adams. It's up $8.7%, almost $23 mil thru late Oct in IRI MULC. Base Belgian White even faster, +11.1%, and intro of White IPA adding a solid $8.5 mil. Factor in better year for Leinenkugel's (+11%) and MillerCoors' super premium biz doing fine. Biggest Leinie brand, Seasonal Shandy, up 2%. Additional $11.2 mil of new Grapefruit Shandy, another shot in arm. Throw in Saint Archer's biz (more than doubling this year) into MC picture and these 4 brand families represent well over $460 mil in sales in IRI MULC.

AB Carving Out Space, Over $200 Mil in Sales Between Sierra Nevada (+22%) and New Belgium (+2%), AB's growing portfolio of high-end craft acquisitions balancing losses for super premium Shock Top brands. All 5 brands AB bought posted solid growth in IRI's off-premise data. Goose Island leads, natch, +31%, almost entirely on back of big push behind IPA. Former flagship 312 Urban Wheat -4% thru Oct 25 this yr. Elysian up solid 38%, a bit faster than 30% growth for 10 Barrel. Blue Point got fastest growth, up near 60%, while Golden Road chugging along +24%. But $18.5 mil in growth from these brands partly offset by declining Shock Top family: -7.7%, $10.9 mil.

Gambrinus Up Solid 8%, CBA +4% Within Gambrinus, Shiner having a good year, +9%, $9.1 mil YTD thru Oct 25. Nearly all of its growth comin' from Shiner Bock and relatively new Ruby Redbird Lager. Meanwhile BridgePort brands still struggling, down 21%, while Trumer Pils up solid 23% YTD. So Gambrinus portfolio still about $10 mil bigger in IRI MULC than CBA's portfolio of brands, which in turn just slightly larger than Lagunitas. Strength of Kona (+16%) and Omission (+21%) continued to buoy CBA (+4%), balancing the basically flat Widmer Bros and a 7% slip from Redhook. Look a little deeper and Kona Big Wave Golden Ale really coming on, +45%, Omission brands solid across the board and Widmer Hefe still up 2%. But Redhook Long Hammer IPA is only growing brand (just barely, +0.3%) in that family, aside from 2 small new entries. Neither KCCO Black Lager nor Audible Ale seem to be sticking in these off-premise channels.

New Brands Keep Deschutes Up Double Digits; Portfolio Strength at Duvel Moortgat, Weakness at NAB Big drop-off before next group of brand families and portfolios. Addition of Firestone Walker to Duvel Moortgat USA's domestic craft biz brings it very close to Deschutes' total sales in IRI MULC thru Oct 25. Deschutes' +10% trend almost entirely due to Fresh Squeezed IPA, nearly tripling this year, and new-intro Pinedrops IPA, adding incremental $1.7 mil. That's as trio of DMUSA brands up near 40% together. That's led by Firestone Walker, +67% by itself. But Boulevard having a better year too, +18%. A bunch of new brands added $1.9 mil to Boulevard growth thru Oct, adding to solid flagship Wheat growth and strong 80% trend for Tank 7 Farmhouse Ale. Speaking of Farmhouse, smallest in DMUSA group, Ommegang, still up 7.5% too.

Almost all of remaining brand families shown above grew thru Oct 25 in IRI MULC data. Clear exception is trio of brand families in NAB portfolio, all of which declined yr-to-date. Largest of 'em declining fastest: Magic Hat down over 11%. Pyramid Outburst IPA up over 20%, but total Pyramid still -6%. Portland Brewing/McTarnahan's is smallest contributor and down 8%.

More Portfolios Coming? Take a peek at the list of brewers that fall in behind the above companies. Six of the next 10 have all made deals funded by private equity firms in the last year or so. Many of those, including Enjoy Beer, which invested in Abita, and the group led by Oskar Blues, have hinted at plans to form larger portfolios of craft brands. So stay tuned and read on.