BMI Archives Entry

However, not all (just mostly) great news for Ballast in latest periods. Sculpin IPA trends noticeably slowed to +21% in IRI supers for latest 4 wks thru Nov 1. A huge slowdown from +100% YTD. Interestingly, while Sculpin IPA, the most expensive top brand by far in supers, has taken pricing down 3.7% to $64.41 per case YTD, in latest 4 wks pricing was closer to flat, at $65.34 per case. Still too early to tell, but Sculpin trends are bound to slow at some point as Sculpin offshoots gain traction. And there's more offshoots comin' in 2016, for Sculpin line and others (see above). If any of those can grow anywhere near the rate Grapefruit shot up, that could certainly make up for any slowdown in original Sculpin, if that even persists.

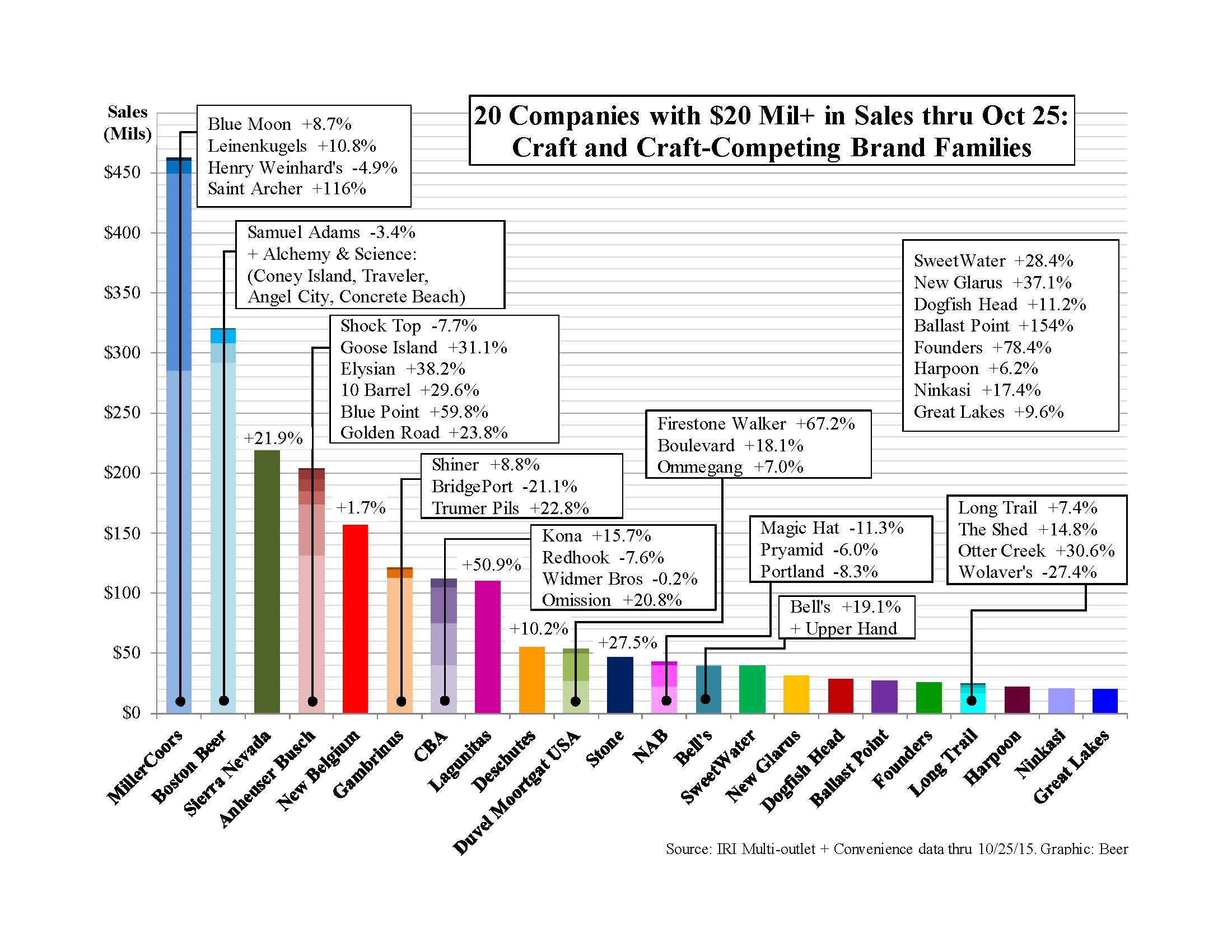

Constellation's Craft "Catch of the Day" Is Biggest Craft Deal Yet; Buys Ballast Point for $1 Bil

Constellation Brands "Catch of the Day," quipped CLSA's Caroline Levy. She said Ballast Point is "one of the most well-regarded craft brewers." Plus "this is the right time for Constellation to get into craft, and though the price is high, Ballast gives it a scalable brand that will help move" Constellation's high end beer portfolio "further up the value chain." Constellation stock up 2% on news today.

Constellation Gets "Crown Jewel" With this deal, Constellation instantly catapults itself into major leagues as a craft player, buying "literally the crown jewel of craft," Constellation ceo Rob Sands told INSIGHTS. It is "by far the fastest growing major craft brewer." Indeed, Ballast Point is more than doubling in 2015. It sold 123,000 bbls last yr and expects to sell about 4 mil cases, or 280,000 bbls in 2015. That's growth of about 128% and would mean Ballast Point would jump from #27 to very near our top 10 in list of craft brewers. Like Lagunitas, it will no longer be part of Brewers Assn list of craft brewers starting with 2016 data. That list has suffered a couple of body blows this yr. Between those 2 brewers, it will lose 1.1 mil bbls of fast-growing craft volume, over 5% of 2015 segment volume and about 15-20% of its 2015 growth.

Calif Gold Rush Continues; Near $2 Bil in 2015 Deals Alone; Each of Top 4 US Suppliers Bought In Three of 5 biggest craft brewers in state did deals this yr: Lagunitas, Firestone Walker and now Ballast Point. So did a coupla much smaller ones: Golden Road and St Archer. We figure almost $1.9 bil spent in them thar hills for craft brewers so far this yr. Howzzat? Yup, $1 bil on Ballast Point, $450-475 mil for half of Lagunitas, $250 mil for Firestone Walker, $100+ mil for Golden Road and $35-40 mil for Saint Archer. Not only that, but each of the top US beer suppliers bought into craft in Calif. Heineken bought half of Lagunitas, Constellation bought Ballast Point, MillerCoors bought St Archer and AB bought Golden Road. Firestone Walker sold to another foreign brewer seeking bigger presence in US craft, Duvel Moortgat USA.

All of this suggests a craft beer landscape that is changing radically. And at warp speed. It also suggests these companies see a lot of oppy for these brands at home and farther afield.

Ballast Point Enhances Constellation's "Leadership" in High End Growth Ballast Point "by far one of the most premium, premium" craft brewers, added Rob, "almost astonishingly so." Recall, Ballast Point gets $356 per bbl, almost 60% greater than Boston Beer. Adding Ballast Point will enable Constellation's continued "leadership" in bringing "greatest amount of growth at retail" and to distribs in high end. Constellation wanted to become a "player in this very fast-growing and important segment" of the beer biz.

Ballast Point Will Stand Alone; Expanding; New Products; No Distrib Changes Ballast Point will continue to operate as a stand-alone unit, said Ballast Point's chief commercial officer Earl Kight. It will expand rapidly from its current 30 states, having just entered KY and Missouri, other states soon to follow. It will be "business as usual," changing distribs "isn't in the plans," said Rob. Ballast Point has rich pipeline of new products coming in 2016, including Pineapple Sculpin, Mango Even Keel (session) and Watermelon Dorado (double IPA). All 3 were featured at LA beer week and in Ballast Point's taprooms for national IPA day and got enthusiastic responses, added Earl.

Ballast Point Is "Extremely Synergistic" With Mexican Import Portfolio; "A Powerhouse" Between Ballast Point and Constellation Brands Beer Division, Constellation will have a helluva 1-2 punch to go to market with, especially in its core Southern California mkts. The Ballast Point portfolio will be "extremely synergistic" with Constellation's portfolio of Mexican import brands, said Rob, pointing particularly to mkt like San Diego, where Ballast Point is a "major, major supplier" and it's "absolutely critical" mkt for Constellation Brands Beer Division as well. Over 1/4 of Ballast Point volume is with Reyes Beverage Group and RBG is also Constellation's #1 wholesaler by far. To "combine those 2 portfolios," emphasized Rob "is a powerhouse like nothing else in revenue and profits. This is what the Gold Network is all about."

A Note About Valuation: Over $3500 Per Bbl; 30+X 2015 EBITDA? Constellation said that it's paying mid-to-high teens multiple of earnings, but that's of "projected 2016 EBITDA." It's in range of 30X 2015 EBITDA. Stifel's Mark Swartzberg estimated that Ballast Point's 2015 EBITDA would be $32 mil. That would make over 30X this yr's earnings. Stifel also estimates that EBITDA will nearly double to $58 mil next yr, leading to a multiple in range that Constellation suggests, 17.2X next yr's EBITDA. Recall, Ballast Point had operating income of $25 mil for 9 mos thru Sep in its amended S-1 filing, back when it was gonna go public. That's ancient history; it filed its S-1 almost a month ago. Something happened since those heady days. Constellation offered a billion reasons to walk away from the initial public offering.

Looks Like A New Day and New Job at Constellation Just this time last week at Beer INSIGHTS Seminar, Constellation CMO Jim Sabia answered question about when his company will buy a craft brewery. Jim pointed to previous comments from Rob Sands and Constellation Brands Beer Div prexy Bill Hacket that "we're in the high end. If the opportunity presents itself, then we'll have some discussions. Right now Job 1 is continuing to focus on our portfolio." Seven days and $1 bil later, Constellation has already changed the story, and the craft landscape. Jim also talked a bit about Constellation's craft collaboration brand Tocayo, developed by celeb chef Rick Bayless and brewed by Chi's Two Brothers as a "test and learn" project. "Is it going to be a big brand today, tomorrow? Maybe, maybe not. However, 5, 10, 15 years from now, if we keep at it, we do the right thing…you just never know." Tocayo is Constellation's first new beer brand. "We're going to take it slow. We're going to learn. We're going to test and learn."

Constellation Brands Buys Ballast Point for Approximately $1 Bil. Just announced. Details to follow.

This week's MegaBrew news offers a wealth of opportunities, and not just for the top two global brewers. Most media outlets needed to find some way to cover the largest beer deal of all time. So ABI's announcement on Wednesday that it formalized an offer to acquire SABMiller (and the multi-month-long dance that led to it) turned into a one-of-a-kind opportunity for interested parties to share their views and extend their influence on consumers and policymakers alike. When your story hinges on independence, what better time than now, with so many listening, to tell it?

Especially outside the biz press, many of the stories written this week do focus on independence. Comments from industry members, advocates, attorneys and writers repeatedly question this deal while advocating the explicit goal of maintaining craft access to market via an independent distribution tier. On its face, this deal has no direct impact on the current structure of beer distribution in the US. However, many observers still insist that scrutinizing this deal should involve challenges to ABI's US distribution, first to any expansion of its wholesaler branches and second, its influence over its independent distributors.

Deal Structure: $108 Bil for SABMiller, $12 Bil for 58% of MillerCoors Plus Global Miller Biz On Wednesday, ABI confirmed its formal $108-bil bid for SABMiller at the same time it announced that Molson Coors plans to buy the 58% of MillerCoors that it doesn't already own for $12 bil. This was the outcome many expected, even though the final price for SABMiller's stake in MC was at the high-end of the range suggested over last few weeks. Molson Coors deal also includes all of MC's US biz, including Redd's, Peroni, Pilsner Urquell and more, as well as about 2.7 mil bbls of Miller brands sold outside the US. The hope, it seems, is for these divestitures to smooth the path toward regulatory approvals that ABI needs in the US and elsewhere.

Even So, "Concerns" Abound: BA and NBWA Advocate for Indie Distribs; Antitrust Attys Weigh In The simultaneous announcements did not stop the steady flow of commentary from politicians and antitrust attorneys, nor industry advocates. In the wake of the deal, leaders of both the Brewers Assn and NBWA issued statements on the proposed deal. Both pledged careful review or analysis of the deal's terms while leaning heavily on their shared interest in an independent middle tier.

"Even with the divestiture of the MillerCoors joint venture," a bigger ABI "has many ramifications" for the US biz, BA CEO Bob Pease wrote. While he described "an independent and competitive middle distribution tier" as "vital" for craft, NBWA CEO/prexy Craig Purser promised his org "will continue to advocate for the open and independent system" of distribution in the US, as well as "for the state-based system of alcohol regulation." Digging a bit deeper into potential impacts of the deal, Bob suggested that it would give the new company "greater influence over commodities used in brewing."

Similar statements from small brewers and the BA's Bart Watson appeared throughout media coverage this week. AdWeek's writeup quoted Bart at length, including bringing up the possibility that other tie ups (like an eventual Heineken/Molson Coors deal) could appear. At the same time, US Senators Ron Wyden (OR) and Chris Murphy (CT) echoed those concerns over access to distribution and raw materials like cans or hops. On the other hand, some small brewers have recently suggested to us that this may not be so much of a problem. Indeed, we've heard a couple times this week that hop growers in PacNW that switched acreage to aroma hops for craft brewers from bittering hops largely bought by brewers like ABI not looking to switch back to accommodate the world's largest brewer. At our Beer Insights Seminar this week, Tony Magee of Lagunitas specifically named large Wash-based Roy Farms as an example of a grower that said "no" to ABI this year.

Various members of the large American Antitrust Institute advisory board continue to offer their legal views of the deal. An extensive examination from experienced antitrust atty Andre Barlow insisted that "consumers will lose" and argued that "the proposed remedies in this transaction, like Modelo, simply aren't enough to prevent a disastrous loss of competition," in post on Law360. He argues that the DOJ should require ABI to sell off its wholly-owned distributorships, as well as prohibit it from "exclusivity pressures" and prevent more branch purchases. He also notes the buying power of the new company in the commodity market and claims "any remedies should take account of this increased purchasing power."

Building Independence Narrative The story of ABI's acquisition of SABMiller is still far from over. But this week's climax came after well over a year of build up that continued to underline these same issues of independence. It was October of last year that ABI sued the state of Kentucky to keep a branch in Owensboro, a few months after state distribs objected to the acquisition. Around the same time, craft entered a period that saw the largest number of acquisitions the segment's ever seen, with ABI an important participant, including at least a couple of deals still in the works. But still, the story we've been telling in this publication since its inception continues too: small brewers, by and large, keep growing and gaining share of beer.

New On-Premise Data Shows 11% Keg Waste in Oct; IPA Leading Style; Bell's Ranks Extra High

New data service, SteadyServ Technologies, measures real-time depletions and sales info using iKeg draft measurement on premise from "a body of retailers" that cover 11 states across the country - NC, SC, FL, KY, OH, IN, MI, MN, NH, TX, and CA. Keep in mind, it's still early days, and therefore a relatively small sample size. During month of October 2015 it measured approx 3.4 mil ounces (or 1720 bbls) poured and sold, with 375,463 ounces (189 bbls) that "went unsold through waste." That's 11% of total beer poured that went unsold thru waste. "Average draft beer was on tap 15.89 days" and retailers on average had 28 taps (tho ranged from 8 taps to 164 taps).

In terms of style, IPA led the way with most ounces poured, 269,632, which accounted for 7.9% of total sales in Oct. That's followed by Light Lagers (5.9%), Light Pilsners (4.7%), Craft Pilsners (3.8%) and Pumpkin beers (3%). Sorted by company, ABI and MillerCoors are largest by far. Yet surprisingly, Bell's is next largest in this set of data, which seems to skew heavier in Midwest. In fact, its Two Hearted Ale is 3d largest brand in terms of ounces poured, only behind Bud Light and Miller Lite. So it's larger in volume than Coors Light, Blue Moon, Guinness Draught, etc.

Alchemy & Science Is Top-25 Vendor in IRI; Keepin' Total Boston Beer Above Water for 4 Wks

Boston Beer subsidiary Alchemy & Science sales shot up $27.3 mil, over 900% YTD thru Nov 1 in IRI multi-outlet + convenience channel. That makes it #24 largest vendor by $$ (if counted separately from Boston Beer). Large part of that is driven by Coney Island Hard Root Beer, natch, which tacked on another $4.3 mil in sales these latest 4 wks to reach $17 mil yr-to-date. Most of the rest comin' from Traveler Beer portfolio top brands - Curious Traveler, Tenacious Traveler and Jack-O Traveler (see Nov 6 issue) while Coney Island traditional beer brands, Angel City and Concrete Beach all growin' fast off of small bases. Interestingly, without including A&S, Boston Beer volume down 5%, $$ down 3% for 4 wks, as each of its top Sam Adams brands (and several others) continue to decline, and new Sam Adams innovations haven't been able to offset trends. Also, Angry Orchard continues to slow (Crisp Apple declined in each of the last two 4-wk periods, tho still +19% YTD). But altogether with A&S, Boston volume up 2%, $$ up 5% for 4 wks, and yr-to-date A&S boosts total trend an extra 4 pts to volume up 10%, $$ up 13% - still good growth for a company their size.

Shiner Bock (and NYFRB) Pass Boston Lager as #3 Brand in Scans Goes to show just how much beer biz is changing these days. Boston Lager $$ sales again dipped 10% for latest 4 wks. Now down 6% YTD thru Nov 1. At same time, Shiner Bock, up 4% for 4 wks and 7% YTD. It has now passed Boston Lager as 3d largest craft brand in scans. It's been steadily growin' mid-to-high single digits all yr, and also passed New Belgium Fat Tire (currently down 2% YTD) earlier in the yr. Meanwhile, Small Town Not Your Father's Root Beer also passed Boston Lager sales YTD with another $16.2 mil in latest 4 wks, to $75.3 mil YTD. It's only just behind Shiner Bock for the yr, and will likely blow past it by next batch of data. Not to mention, after just recently launching its new canned 6pk, that's already the 30th best-selling package in IRI MULC (NYFRB 6pk in bottles is #1 craft pkg YTD). Sure woulda been difficult to imagine Boston Lager sales surpassed by Shiner Bock and an alc Root Beer before this yr. Though both Coney Island and NYFRB markedly slowing in recent weeks, CBN understands.

Sierra Slowdown in Oct After strong September in scans with extra boost from its new Oktoberfest, Sierra Nevada growth notably slowed for latest 4 wks thru Nov 1 in IRI MULC. Total company $$ still up 14% in latest period, and +22% YTD. Yet Sierra Pale down 2% for 4 wks, Torpedo IPA slowed to +2% (volume slightly down) and Sierra Variety Pk down 6% for 4 wks. Each of those brands still healthy yr-to-date. Sierra Seasonal still rockin', up 41% for 4 wks, 20% YTD. And both Hop Hunter and Nooner Pilsner intros continue to provide big lift in sales this yr - last tallied at a combined $17.2 mil YTD thru Oct 25 (see Nov 6 issue). But there too perhaps change is in air; someone sent CBN a picture of Hop Hunter on sale for $4.99/6-pk.

You can't know where you're going if you don't know where you've been. We built our latest special report with that adage in mind, providing for the first time an in-depth look at the US beer industry from 1980-2014. This new digital-only report that we're calling The Long View becomes available next week. Pre-order now to be among the first to benefit from its exclusive look at 35 years of beer stats including total US shipments, major brewer and importer trends, segment and brand data and much more. See how US taxpaid shipments barely changed, their 2014 level almost identical to 1981. Read about the rise of today's lead brands, the growth of imports and decline in per capita consumption. A combo of in-depth text analysis that only BMI's experienced editors could compile, full data sets for 35 years and 30 color graphs and charts, the 100-pg digital report offers a detailed look at how the beer industry has grown and changed since 1980. Seek out more information and pre-order your copy of The Long View today for $249 to receive it when it becomes available next week.

Pace of new brewery openings in Denver is "finally showing signs of a slowdown" in 2016, according to recent Westword article. Tho that's partly 'cause new breweries have been opening left and right in recent yrs. By the end of 2015, number of breweries in the city will have jumped from 8 to "more than sixty," as total of "at least eighteen" breweries will open by year end - a new annual record vs 16 last yr. So Denver's averaging "more than one per month in the last 2 years." Yet "2016 doesn't look like it will keep a comparable pace," (or anywhere close), sez paper. Only "brand-new" brewery expected to open next yr is Briar Common Brewery + Eatery, which originally planned to open this year, before it "pushed construction out into 2016." Then paper lists Blue Moon's pilot brewery, expected to open in 2016. And the others listed - Great Divide's production brewery, New Belgium pilot brewery, and a potential brewery "inside the Westin Hotel at Denver International Airport" - aren't expected to open until 2017. "Beyond that? Crickets," sez paper. "Still several would-be breweries in the planning stages scouting the city for a location," yet none have "signed a lease or even zeroed in on an address." There are however, "several breweries slated for suburban communities, such as Lakewood, Evergreen, Castle Rock, and Aurora." This has already been happening across the country to an extent, but it's possible that next wave of new breweries in CO (and across the US) are increasingly lookin' to less crowded, less competitive areas, or perhaps simply less expensive.

Starting tomorrow 21st Amendment Brewing will expand to southern NV with Wirtz Beverage, co announced. This marks its 4th new state entered this year, including recently entered FL, as well as Chicagoland, IL and NH earlier this yr (also partnered with Stone Dist in SoCal and Central Coast region this May). 21st Amendment entered Jacksonville area, FL with Champion Brands in late September/early October, will expand to "a few other parts of the state" by the end of the yr, and expects to fill out FL by early 2016, co confirmed with CBN. So it seems 21A's lookin' to put extra capacity at its new brewery to use. In NV it'll start in five counties - Clark, Esmeralda, Lander, Lincoln and Nye - with El Sully Mexican Lager, Down to Earth Session IPA, Brew Free! Or Die IPA, Back in Black Black IPA, Fireside Chat Winter Ale, Good Things Belgian Triple, and new Toaster Pastry India Red Ale.

Meanwhile, 21A lookin' solid in natl scans with just a couple mos to go in 2015; $$ up 44% in IRI multi-outlet + convenience thru Oct 25. All growth and more comin' from its Seasonal (+85%), Brew Free or Die IPA (+37%) and Down To Earth Session IPA (incremental $490K) this yr, while co phases out Bitter American Session.

Oct Craft Brewer Distribution Territory Expansions October was a more active mo for craft brewer territory expansions, with at least 27 different breweries that entered or changed distribs in 36 new mkts. In case you lost track, we've put 'em all together for you in one handy pdf. Organized by state, this list includes craft brewer distribution expansions with sales expected to begin in Oct 2015, as well as a preview for Nov 2015 expansions. While it may not be comprehensive, this list includes announcements made by the largest craft brewers and many expansions by smaller players.